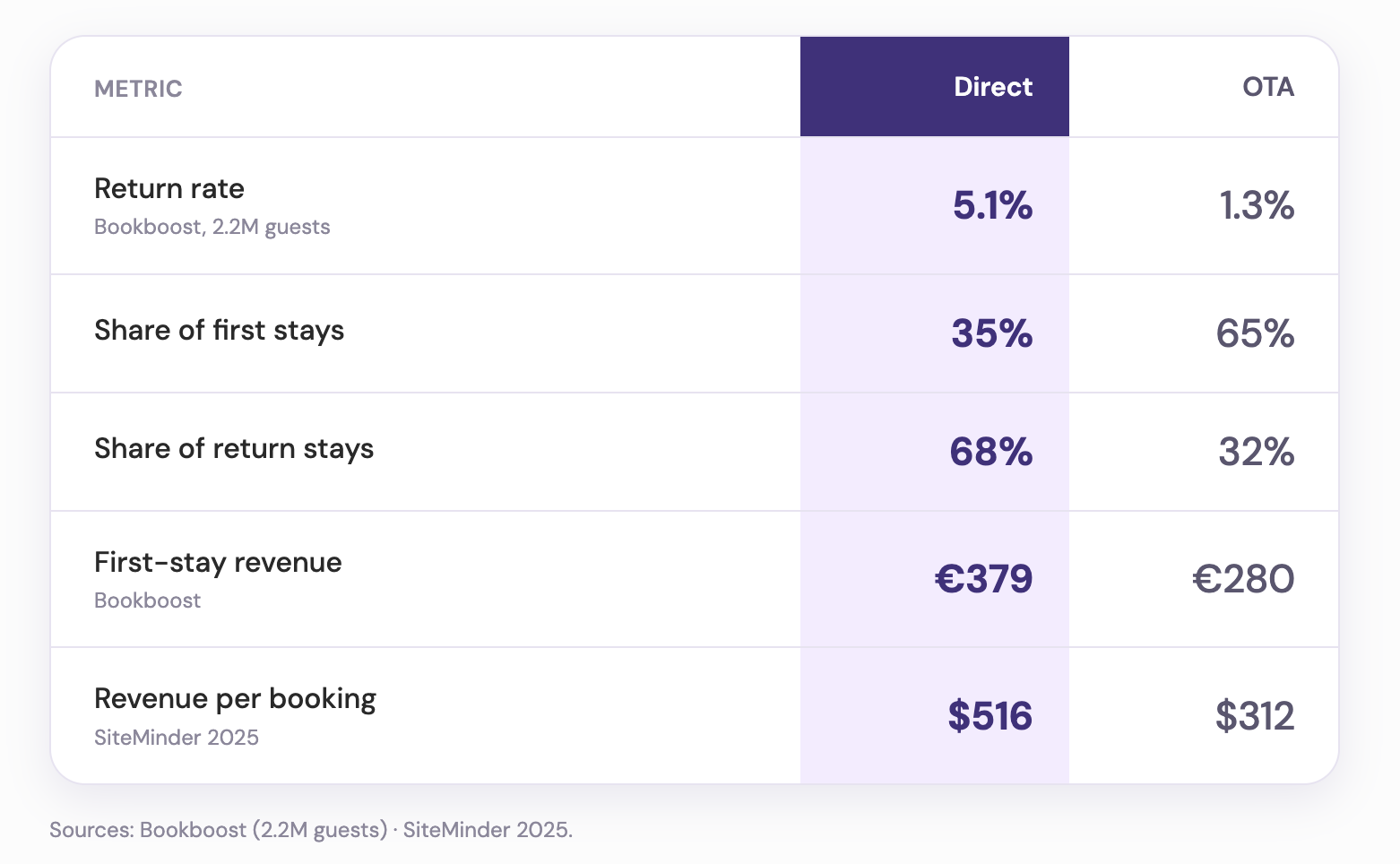

A guest who books direct returns at 5.1%, while a guest who books through an OTA returns at just 1.3%, and that gap holds across the same hotels, the same rooms, and the same front desk teams. That is close to four times the return rate, and it is set before the guest ever checks in.

The figure comes from a Bookboost analysis of 2.2 million guests at European hotel groups between 2024 and 2026, and it reflects real booked and re-booked behaviour, not survey answers. Here is why the gap happens, what it costs you, and what to do about it.

The headline ratio sits inside a deeper pattern. When you look at first stays across the same 2 million-plus guests, OTAs account for 65% of them and direct accounts for 35%, which will not surprise anyone who reads a P&L.

Now look at return visits to the same properties and the mix flips: OTAs drop to 32% of repeat stays while direct climbs to 68%. The acquisition channel that brought most of the volume in the front door brings less than a third of the volume back.

This is the trap European hoteliers have been priced into. HOTREC's 2024 European Hotel Distribution Study put direct at 50.9% of overnight stays in 2023, with OTAs at around 30%, so at the European average direct still leads. But that average hides the independents: Phocuswright found OTAs captured 61% of bookings for independent properties in 2024, so smaller and mid-sized operators are paying a tax they have come to treat as fixed. It shows up as commission, and more quietly as a return-rate gap nobody has been measuring. As a Commercial Director at one of our customers put it, "We pay 18% to Booking.com and they own the guest relationship."

A guest who books through an OTA gets confirmation, support, the post-stay email, and the next ad all from the OTA, while the hotel receives a name, a stay window, and, if it is lucky, an email address that has not been masked. Everything that builds a return habit happens on someone else's platform.

A direct guest is different from the first click, because they have already consented to be marketed to. They land on the hotel's website or app, and the property keeps the post-stay guest journey, so the next booking starts with a search bar the hotel owns.

This is not just our read of the data. Skift Research found more than 80% of hoteliers believe direct guests are likelier to return, and forecasts direct digital bookings to overtake OTA gross bookings globally by 2030, at more than $400 billion versus $333 billion. The shift is coming, and the question is whether your repeat-rate data is ready when finance asks why the budget is moving.

.jpg)

Retention is only half the picture; revenue is the other half.

Bookboost data shows direct-acquired guests generate 35% more revenue on the first stay than OTA-acquired guests, at €379 versus €280 across the European mid-market sample, before any commission is deducted.

SiteMinder's 2025 Hotel Booking Trends report, which measures revenue per booking through the channel manager, found hotel websites generate 60%-plus more per booking than OTAs, at $516 versus $312. Two different sources measuring different things arrive at the same place. Direct guests spend more because they book longer stays, add more on property, and sit at higher rate codes, rather than arriving through the discount-led shop window of an OTA listing.

Stack commission on top and the gap widens. A €280 OTA stay at 18% commission nets the hotel €230; a €379 direct stay nets the full €379, minus a fraction of CPC that rarely approaches OTA economics even at expensive Google Hotel Ads rates. As a GM running a four-property European group put it, "OTA commissions are eating us alive." Every percentage point of OTA dependency compounds across rate, retention, and margin.

The Bookboost and SiteMinder rows measure different things in different currencies, so do not read them as a direct comparison. Each one simply shows direct earning more than OTA within its own dataset.

The pattern across all five rows is the same: direct guests are worth more on the first stay and more again over time.

Among guests who stay 10 or more times, the gap stops being a multiple and becomes a category difference. Direct-acquired loyal guests generate around €3,000 in cumulative revenue over their lifetime with the property, against around €985 for OTA-acquired loyal guests, roughly 3x.

One caveat, and it points the right way. The OTA sample at 10+ stays is small, only 121 guests, because almost no OTA-acquired guests get there at all. That is partly the point: the reason they are rare in the loyal cohort is the same retention gap that opened on stay one. So treat the 3x as a rough signal, not a hard benchmark.

Commission is a cost you can see in the P&L. Retention liability is the one you cannot: the guest you paid 18% for comes back to the city next year and books a competitor through the same OTA, because that is the surface they trust. That second booking never lands on your books.

Mid-market European groups can absorb the commission, but not a lifetime-value gap that runs 3:1 against direct over a decade. The job is not to ban OTAs but to treat every OTA stay as the start of a conversion, not the end of an acquisition.

.jpg)

These are the moves Bookboost customers run, ranked by how often they pay back inside a quarter.

1. Pre-arrival upsell with a direct identity. Send the room upgrade, the parking add-on, and the spa slot from the property's own communication channel before check-in, so the guest now has a conversation with the hotel rather than the OTA.

2. Post-stay direct-rate offer with a short window. Inside seven days, send a personalised offer for a return stay at a rate that the OTA cannot show, time-bound, segmented by trip purpose, and sent from the property's domain.

3. In-app or web booking with a reason to log in. A loyalty programme, a stored preference, a saved payment method, or anything that makes the second booking faster on your surface than on Booking.com.

All three depend on owning clean, consented guest data and being able to act on it inside a single system, which is what a customer data platform is for.

Pull last year's bookings, tag them by acquisition channel, and calculate the return rate for each. If the gap looks like ours, set one quarterly goal: convert 10% of OTA stays into direct repeat bookings within 12 months. Then read our post-stay guest journey playbook for the tactics that make the conversion stick. The guest relationship is yours to keep, so start measuring it that way.

Want more content like this? Get hospitality strategies delivered to your inbox via More Than Bookings, our newsletter that cuts through the noise. Subscribe today!

Are you ready to increase your revenue and build lasting guest relationships? Take the first step today.

.jpg)

.jpg)